Fiscal and Policy Implications of Selling Pipe Tobacco for Roll-Your-Own Cigarettes in the United States

Supporting Files

Public Domain

-

May 02 2012

File Language:

English

Details

-

Alternative Title:PLoS One

-

Personal Author:

-

Description:Background

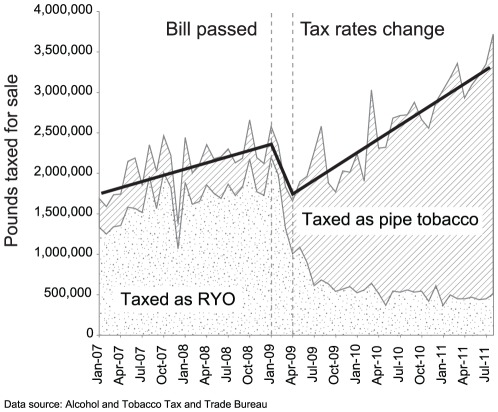

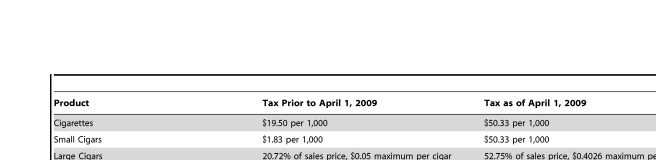

The Federal excise tax was increased for tobacco products on April 1, 2009. While excise tax rates prior to the increase were the same for roll-your-own (RYO) and pipe tobacco, the tax on pipe tobacco was $21.95 per pound less than the tax on RYO tobacco after the increase. Subsequently, tobacco manufacturers began labeling loose tobacco as pipe tobacco and marketing these products to RYO consumers at a lower price. Retailers refer to these products as “dual purpose" or “dual use" pipe tobacco.

Methods

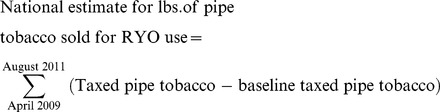

Data on tobacco tax collections comes from the Alcohol and Tobacco Tax and Trade Bureau. Joinpoint software was used to identify changes in sales trends. Estimates were generated for the amount of pipe tobacco sold for RYO use and for Federal and state tax revenue lost through August 2011.

Results

Approximately 45 million pounds of pipe tobacco has been sold for RYO use from April 2009 to August 2011, lowering state and Federal revenue by over $1.3 billion.

Conclusions

Marketing pipe tobacco as “dual purpose" and selling it for RYO use provides an opportunity to avoid paying higher cigarette prices. This blunts the public health impact excise tax increases would otherwise have on reducing tobacco use through higher prices. Selling pipe tobacco for RYO use decreases state and Federal revenue and also avoids regulations on flavored tobacco, banned descriptors, prohibitions on shipping, and reporting requirements.

-

Subjects:

-

Source:PLoS One. 2012; 7(5).

-

Document Type:

-

Place as Subject:

-

Volume:7

-

Issue:5

-

Collection(s):

-

Main Document Checksum:urn:sha256:d6ac2079f2a2520fbb8e4affe3df843b31f6b2478cca325387599ce76055963b

-

Download URL:

-

File Type:

[PDF

- 210.14 KB

]

[PDF

- 210.14 KB

]

Supporting Files

File Language:

English

ON THIS PAGE

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

CDC STACKS serves as an archival repository of CDC-published products including

scientific findings,

journal articles, guidelines, recommendations, or other public health information authored or

co-authored by CDC or funded partners.

As a repository, CDC STACKS retains documents in their original published format to ensure public access to scientific information.

As a repository, CDC STACKS retains documents in their original published format to ensure public access to scientific information.

You May Also Like

COLLECTION

CDC Public Access