Impact of Maryland’s 2011 alcohol sales tax increase on alcoholic beverage sales

Supporting Files

-

7 2016

-

File Language:

English

Details

-

Journal Article:Am J Drug Alcohol Abuse

-

Personal Author:

-

Description:Background:

Increasing alcohol taxes has proven effective in reducing alcohol consumption, but the effects of alcohol sales taxes on sales of specific alcoholic beverages have received little research attention. Data on sales are generally less subject to reporting biases than self-reported patterns of alcohol consumption.

Objectives:

We aimed to assess the effects of Maryland’s July 1, 2011 three percentage point increase in the alcohol sales tax (6–9%) on beverage-specific and total alcohol sales.

Methods:

Using county-level data on Maryland’s monthly alcohol sales in gallons for 2010–2012, by beverage type, multilevel mixed effects multiple linear regression models estimated the effects of the tax increase on alcohol sales. We controlled for seasonality, county characteristics, and national unemployment rates in the main analyses.

Results:

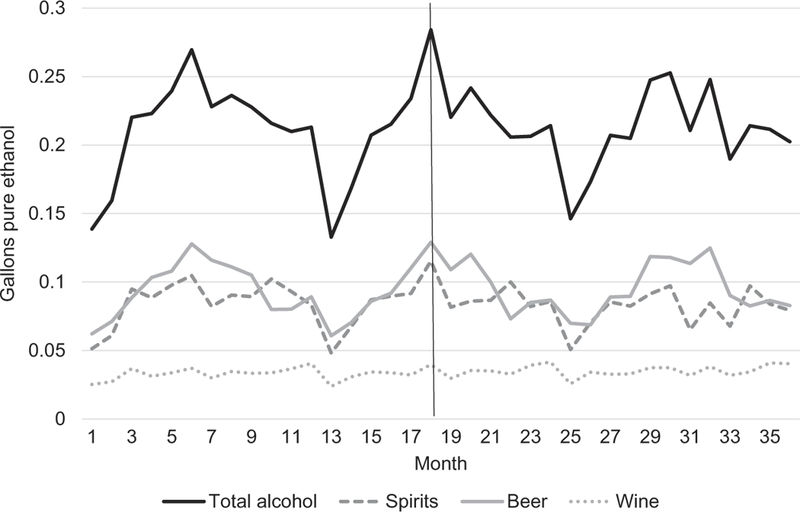

In the 18 months after the tax increase, average per capita sales of spirits were 5.1% lower (p < 0.001), beer sales were 3.2% lower (p < 0.001), and wine sales were 2.5% lower (p < 0.01) relative to what would have been expected from sales trends in the 18 months prior to the tax increase. Overall, the alcohol sales tax increase was associated with a 3.8% decline in total alcohol sold relative to what would have been expected based on sales in the prior 18 months (p < 0.001).

Conclusion:

The findings suggest that increased alcohol sales taxes may be as effective as excise taxes in reducing alcohol consumption and related problems. Sales taxes also have the added advantages of rising with inflation and taxing the highest priced beverages most heavily.

-

Subjects:

-

Keywords:

-

Source:Am J Drug Alcohol Abuse. 42(4):404-411

-

DOI:

-

Pubmed ID:27064821

-

Pubmed Central ID:PMC6438373

-

Document Type:

-

Funding:

-

Genre:

-

Volume:42

-

Issue:4

-

Collection(s):

-

Main Document Checksum:urn:sha-512:42fbebd021aa5eefc706aaa5cc8c3fb211a4a71b821511d06de94f217023bd058da4150db84876c36e19400a1af76774da2de579b38ea24db4b0b746396501b4

-

Download URL:

-

File Type:

[PDF

- 391.81 KB

]

[PDF

- 391.81 KB

]

Supporting Files

File Language:

English

ON THIS PAGE

{kind=link}

{kind=link}

CDC STACKS serves as an archival repository of CDC-published products including

scientific findings,

journal articles, guidelines, recommendations, or other public health information authored or

co-authored by CDC or funded partners.

As a repository, CDC STACKS retains documents in their original published format to ensure public access to scientific information.

As a repository, CDC STACKS retains documents in their original published format to ensure public access to scientific information.

You May Also Like

COLLECTION

CDC Public Access